Political risk—and what firms do about it

From the UK’s vote to leave the European Union to the threats of the US Congress to shut down the federal government, recent events have renewed concerns about the effects of risks emanating from the political system on investment, employment, and other aspects of firm behavior. The size of such effects, and the question of which aspects of political decision-making might be most disruptive to business are the subject of intense debates among economists, business leaders, and politicians. However, quantifying the effects of political risk has often proven difficult due to a lack of firm-level data on the extent of exposure to political risk, as well as a lack of data on the kind of political issues firms may be most concerned about.

In our new INET working paper, we use textual analysis of quarterly earnings conference-call transcripts to construct a firm-level measure of the extent and type of political risk faced by individual firms listed in the United States. The vast majority of firms with a listing on a US stock exchange hold regular conference calls with their analysts and other interested parties, a forum where management gives its view on the firm’s past and future performance and responds to questions by call participants about any challenges the firm may face. Our approach to quantifying the extent of political risk faced by a given firm at a given point in time is simply to measure the share of the conversation between participants and firm management that centers on risks associated with politics in general, and with specific political topics.

To this end, we adapt a simple pattern-based sequence-classification method developed in computational linguistics to distinguish between language associated with political versus non-political topics (Manning et al., 2008). For our baseline measure of overall exposure to political risk, we use a training library of political text (an undergraduate political science textbook or text from the political section of newspapers) and a training library of non-political text (an accounting textbook, text from non-political sections of newspapers, or transcripts of speeches on non-political topics) to identify two-word combinations (“bigrams”) that are frequently used in political texts. We then count the number of instances in which conference-call participants use these bigrams in conjunction with synonyms for “risk” or “uncertainty,” and divide by the total length of the conference call to obtain a measure—which we dub PRiskit—of the share of the conversation that is concerned with risks associated with politics.

After constructing our measures, we present a body of evidence that they are indeed capturing political risk. Firstly, we show that each of our top-scoring transcripts correctly identifies conversations that center on risks associated with politics (for example, concerns about regulation, ballot initiatives, and government funding). Secondly, we find our measure varies intuitively over time and across sectors. For example, the mean across firms of our main measure of overall political risk increases significantly around federal elections and is highly correlated with the index of aggregate economic policy uncertainty proposed by Baker et al. (2016). It is also highly correlated with sector level proxies of government dependence used in the existing literature.

Thirdly, we show that our measure correlates with firm-level outcomes in a way that is highly indicative of reactions to political risk. We use stock return volatility, investment, employment, political donations and lobbying activities as the firm-level outcomes. Standard models predict that an increase in any kind of risk, and thus also an increase in the firm’s political risk, should trigger a rise in the firm’s stock market volatility and decrease its investment and employment growth (e.g., Pindyck (1988); Bloom et al. (2007)). In contrast to these “passive” reactions to overall risk, firms may also “actively” manage political risk by donating to campaigns or lobbying politicians (Tullock, 1967; Peltzman, 1976). Such “active” management of political risks should be concentrated among large but not small firms, because large firms internalize more of the gain from swaying political decisions than small firms (Olson, 1965). Our results are consistent with all these predictions.

Interestingly, we find the incidence of political risk across firms is far more heterogeneous and volatile than previously thought. The vast majority of the variation in our measure is at the firm level rather than at the aggregate or sector level, in the sense that it is neither captured by time fixed effects and the interaction of sector and time fixed effects, nor by heterogeneous exposure of individual firms to aggregate political risk. In this sense, firms considering their political risk may well be more worried about their relative position in the cross-sectional distribution of political risk (for example drawing the attention of regulators to their firms’ activities) than about time-series variation in aggregate political risk.

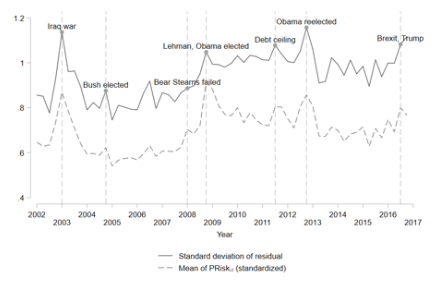

Figure 1: Dispersion of PRiskit over time

A direct implication of these results is that the effectiveness of political decision-making may have important macroeconomic effects, not only by affecting aggregate political risk, but also by altering the identity of firms affected by political risk and the dispersion of political risk across firms. As shown in Figure 1, the dispersion of this firm-level political risk increases significantly at times with high aggregate political risk.

Decomposing our measure of political risk by topic, we find that firms that devote more time to discussing risks associated with a given political topic tend to increase lobbying on that topic, but not on other topics, in the following quarter.